Czech income tax applies to earnings in the Czech Republic. The personal income tax rate is 15% on income up to 1,676,052 CZK and 23% on income above this amount for the 2025 tax year (filed in 2026)

Self-employed individuals (OSVČ) are also required to contribute to social security and health insurance. In most cases, both Czech citizens and foreigners living and working in the Czech Republic must file a Czech tax return. Here’s when and how to file.

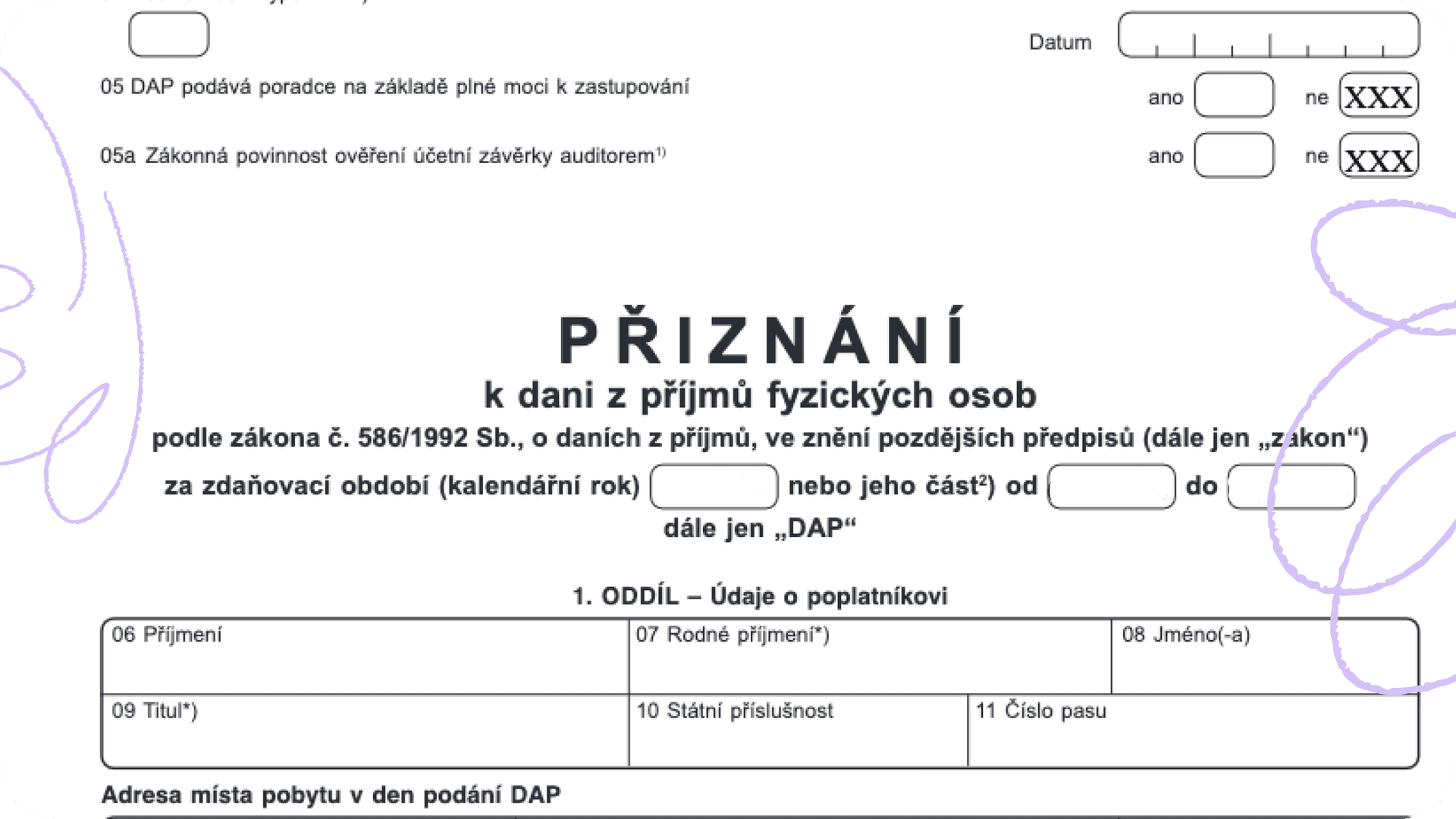

Filing Czech Tax Returns - A Complete Guide for Foreigners

Anybody living and working in the Czech Republic has the obligation to pay income tax once every year. The tax return (“daňové přiznání” in Czech) is common practice for those with an active trade license (Živnostenský). However, it isn’t only freelancers and the self-employed who must file income tax returns. It’s also employees, pensioners, and students.

In 2026, this obligation covered all self-employed persons and entrepreneurs. It also extended to students holding more than one part-time job or doing self-employed business. Some received tax-exempt status, while those with no exemption had to file a tax return for 2025.

Completing a Czech tax return takes into account many factors, from tax benefits and tax rebates to calculating net wage. Filers can also reduce the tax base through charitable donations. If filers own property, they should be aware of how to properly charge real estate tax, or calculate rental income. There can be many variables (and documents) to get right, some which might particularly confuse foreigners and first-time filers.

To learn more, read on for our complete guide to filing Czech taxes. We’ll share who has to file, when to do it, and how to file Czech income taxes properly.

Who has to file Czech taxes?

With so much to cover, let’s break down Czech tax reports for the taxpayer. Who has to file taxes in the Czech Republic?

Active trade license holders (self-employed, in Czech “Živnostenský list”)

Employees with self-employment, capital gains, rent or other taxable income exceeding CZK 15,000 per year

Those working simultaneously for two employers in any one month when both jobs paid income tax in advance

Unemployed persons with capital gains, rental or other income over CZK 50,000 annual

Students who work more than one part-time job or doing self-employed business

Filing deadline for tax returns

The date for filing tax returns in the Czech Republic does not change from one taxpayer to the next. Self-employed persons, as well as employees, pensioners, students, and anybody responsible for reporting taxes all have the same deadline. For submitting the personal income tax report for 2025, the deadline is 1 April 2026.

Typically, tax season and collecting documents for most begins in March. This can change (as we saw over the course of the pandemic), but tends to be around this time of the year.

Taxpayers report income, health & social contributions, and deductibles or tax credits to calculate the remaining balance to pay in taxes.

If submitting tax returns electronically, the deadline is extended by one month. In 2026, this extended the deadline to 2 May. Taxpayers submit reports (whether by mail, in-person or digitally) to the Czech Financial Administration. However, only taxpayers who have income from dependent activities can use the two-page tax form.

How to File a Czech Tax Return?

To file a Czech tax return, follow these methods:

Via Databox – Upload your XML file with tax calculations and personal details.

Tax Office EPO – Calculate income tax, enter personal details, and submit electronically.

Portal Moje Dane – Enter your income details, calculate taxes, and file electronically.

Via Tax Advisor – Hire a tax advisor or accountant to handle your tax calculations and submissions on your behalf

Important: If you're a trade license holder and declaring self-employed (ICO) tax, you must also submit social security and health insurance declarations.

Which tax form to use?

There are two types of tax forms in the Czech Republic:

the standard four-page tax form, and;

a simplified two-page tax form.

Download either of these forms from the Financial Administration website or here, just as in previous years. Keep in mind the simplified tax form is only for those with income from dependent activities. Beyond using one of these forms, taxpayers might also need to collect some important documents.

Important documents to collect

Which documents you need to file taxes will vary depending on whether you’re employed, have a trade license, or both. If you are employed, you need to get a certificate of taxable income(Czech name of the form is Potvrzení o zdanitelných příjmech ze závislé činnosti, sražených zálohách na daň a daňovém zvýhodnění) from the employer. If you worked for multiple employers in the last tax year, then you should get the forms from each of them.

This is more straightforward than filing taxes as a freelancer, who should compile all invoices from the given tax period.

Trade license holders must file taxes according to a flat-rate (60/40) expenses or real expenses. Apply these as expenses related to your business, which will later be deducted from the remaining balance owed in taxes. When choosing to file using flat-rate expenses, there is no obligation for filers to keep records of invoices or receipts.

If filing taxes using real expenses, which is sometimes more advantageous, there’s documentation to do. The person filing should keep records of all costs paid for the entire year. They must keep receipts for at least 3 years. Anything related to conducting business can apply as an expense, however with numerous exceptions.

What can you write off as business expenses?

Some costs you can write off as real expenses include:

Vehicle expenses (under certain conditions, e.g. road tax registration)

Royalties

Management service fees

Interest charges to foreign affiliates

Technology you purchase to use in your business (e.g. work computer)

Office rental for conducting your business

The Czech company will have to prove these costs meet general rules for tax deductibility, however.

NOTE: You can not combine tax methods 60/40 and real expenses. You should always choose one of them.

Exceptions to real business expenses

What doesn’t count as real expenses when reporting taxes in the Czech Republic?

Cost of food

Beverages and refreshments

Dining at restaurants

Advances to Social Security

Contributions to Health Insurance

Note: social and health advances cannot be written off as business expenses. This is because all taxpayers must prove their advances to pension insurance and to health insurance. This information is available through the respective offices at the end of the year.

Health insurance providers tend to send this automatically, while Social requires access via an e-identity / e-portal system.

Most common deductibles

Now, when filing, you’ll also want confirmation of deductions. The most common deductions are mortgage interest, donations, pension insurance, and life insurance. Filers can prove payment to any of these via confirmation from a bank, insurance provider, or other means. Other common deductibles include the following.

Dependent children or child (claimable by only one of the parents)

Deductions for a non-working spouse (whose income does not exceed a certain limit and takes care of a kid under 3 years)

How to submit an Employee tax return

Employees over the course of a tax calendar year must file a tax return if they had:

Income from self-employment;

Capital income;

Rental income, or;

Other taxable income exceeding CZK 15,000/month (see note below).

Employees can submit an Employee tax voluntarily due to bonuses.

Voluntarily for deducting tax reliefs and bonuses and getting tax refunds.

Note: You must submit a tax return even if working for two different employers who both pay advance income tax. (If income exceeds CZK 15,000, the employee must file a tax return.)

Examples of Czech employee tax returns

To avoid any confusion, we’ll share some examples of who should file an employment tax return in the Czech Republic. If any of these match your situation, you will not be able to apply for an employer annual tax statement.

1 - Were you employed with a brigada?

If you worked for a brigade earning income throughout the year from more than one company, you may have to file. For example, say you worked for employers on a classic employment contract. These employers paid a gross monthly salary of CZK 40,000. Then, to earn additional income, you work on contract for employers, whose pay you receive on top of AB’s.

At this point, if you earn taxable income from more than one employer in the same month, you must file. You cannot apply to any of the employers for an annual tax settlement.

2 - Have you been self-employed for part of the year?

Next, say you conducted self-employed business for only part of the year, from January to November. Your business began in December, giving you only one month with very minimal, taxable income, say CZK 10,000. In this case, you cannot apply for the annual tax settlement from the previous employer. You must file a Czech tax return for any income from self-employment.

3 - Did you do any part-time work?

If you worked for two part-time employers in the Czech Republic, you are obliged to file a tax return. Now, because this income comes from dependent activities only, you can use the simplified two-page tax form. This is according to § 6 of the Income Tax Act. To complete the tax return, you will however need a certificate of taxable income from both employers.

4 - Were you employed and with rental income?

In addition to employment income, if you earn anything from rentals (i.e. an apartment), you file a tax return. In this case, you will need to use the standard 4-page tax form as well as appendix number two of the return. Here, rental income according to § 9 of the Income Tax Act can be reported along with employment income.

5 - Are you an entrepreneur while on pension?

If yes, here we need to get into some numbers. Say, for example, a retired pensioner was self-employed for the taxable year at an annual income of CZK 450,000. All expenditures apply at a 60% flat rate, bringing the annual tax base to CZK 180,000. On this 180,000, the entrepreneur must pay taxes.

However, it will be excluding contributions to social and health as well as any tax bonuses or discounts.

In this specific case (in 2025), the basic discount available to all taxpayers was CZK 30,840. This number changes from year-to-year, but let’s use it for example. The tax discount decreases tax liability, which before the discount is 15% for this entrepreneur.

If income tax before applying the discount is equal to or less than the rebate, annual tax liability becomes zero. And here, it is. This means you won’t have to pay any personal income tax, but you still must submit and fill in a tax return.

How to calculate Czech personal income tax

There are two income tax brackets in the Czech Republic for the 2025 tax year (filed in 2026): 15% applies to income up to 1,676,052 CZK, and 23% applies to income above this amount.

There are also non-taxable items (tax deductibles) to reduce the tax base if certain legal conditions are met. Most commonly, these include: gifts, housing interest, advance deposits on pension insurance savings, or life insurance. For the lower tax base, each CZK 1,000 in rebates amounts to CZK 150 in savings. While for the higher tax base, it’s up to CZK 230 per 1000.

Want to get an estimate on your taxable income and what you’ll be paying? Try Pexpats’ free tax calculators!

Tax rebates to reduce income tax

If you’re entitled to any tax deductions, deduct these from your calculated personal income tax for the year. For the 2025 tax year, each taxpayer had a taxpayer discount of CZK 30,840. Beyond this, other discounts include:

Spouses with independent income who is taking care of kid under 3 years old and not exceeding CZK 68,000 (discount of CZK 24,840 in 2025)

Also spouses with independent income under CZK 68,000 holding a ZTP / P card (49,680 crowns)

First and second-degree disabilities (CZK 5,040)

ZTP / P card holders (16,140 crowns)

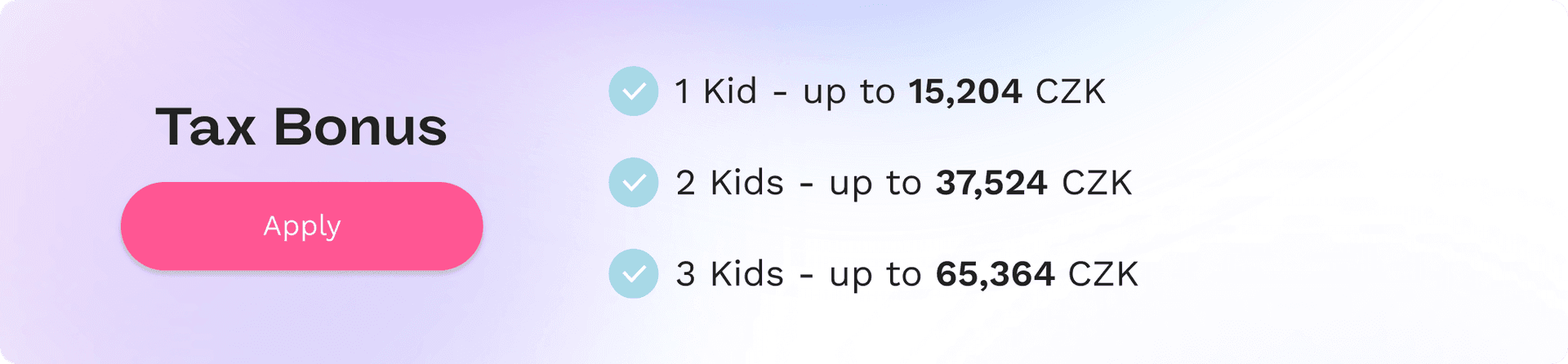

Also, parents can claim tax benefits for their children. In this case, the annual benefit allowance for 2025 is CZK 15,204 for the first child. For the second, it is 22,320 crowns, while for the third and subsequent children CZK 27,840.

If the child also holds a ZTP / P card, then you can apply for double the tax benefit.

Who is eligible to receive the tax bonus?

Taxpayers claiming benefits for children are not required to pay income tax, and even receive money from the state. This money comes in the form of a tax bonus, but only when the tax benefit exceeds the calculated income tax.

Example of tax bonus entitlement

Say you’ve earned a gross annual profit of CZK 500,000 and claim a tax benefit for 3 children. The benefit in this case comes to a total of CZK 65,364 (15,204 + 22,320 + 27,840). Now, here, you will claim only the basic taxpayer rebate along with the aggregate discount for the three children. You cannot claim any other rebate or non-taxable item, however.

The income tax calculation will thus come to CZK 75,000 (500,000 x 15%). After deductions for the taxpayer discount, CZK 44,160 remains (75,000 - 30,860). Now, apply the benefits for the three children, and you’re entitled to CZK 21,204 (44,160- 65,364).

Should I register for VAT or Light VAT?

Anybody whose annual turnover exceeds CZK 2.5 million must register as a VAT payer. Value Added Tax (VAT), or in Czech “daň z přidané hodnoty” (DPH), is officially known as the European Reverse Charge. What this means is that you will not charge European-business clients VAT. It does not mean that you will pay any additional VAT.

Also, if you invoice any EU-business client who pays VAT, you must register for Light VAT. VAT Light (“identifikovaná osoba”, in Czech) must be applied for through the local tax office (finanční úřad).

Flat tax rate - advantages and disadvantages

Now, in 2026 the Czech government introduced a flat tax rate (“paušální daň”). Taxpayers who apply for the flat rate pay only a monthly advance (in 2026, CZK 9,984). This amount covers both social and health insurance, as well as CZK 100 advance to income tax. There is no filing at the end of each calendar year and typically less hassle overall. VAT payers, full-time employees, and those with self-employed activities cannot apply for the flat rate.

For foreigners, applying for a flat tax rate isn’t always advantageous, however. For one, a tax assessment for filing taxes with a home country is impossible. This is because no annual statement is filed, making it extremely complicated to prove income to foreign authorities.

It also makes it impossible to obtain tax residency status, and in some cases, avoid double taxation from countries requiring it.

Czech Tax Return Application and Payment Deadlines for 2026

The Czech income tax deadlines for the 2025 tax return filed in 2026 depend on how the return is submitted. The same deadlines apply for both submission and payment of the tax.

Overview of Czech Income Tax Filing and Payment Deadlines (2026)

Submission Type | Tax Return Deadline | Payment Deadline | Requirement |

|---|---|---|---|

Paper submission | 1 April 2026 | 1 April 2026 | Standard filing |

Electronic submission | 4 May 2026 | 4 May 2026 | Filed online |

Via tax advisor | 1 July 2026 | 1 July 2026 | Power of attorney submitted by 1 April 2026 |

Source: Finanční správa ČR

If a tax advisor submits the tax return, the deadline is automatically extended to 1 July 2026, but only if the power of attorney is delivered to the tax office by 1 April 2026.

For trade license holders (OSVČ), additional obligations apply after submitting the income tax return:

Social security and health insurance reports must be submitted

Any balances must be paid based on the submitted reports

New monthly deposits are set based on the reported income

In practice, the Czech tax process includes income tax submission, insurance reporting, and payment obligations, all of which follow the official deadlines set by the Czech Financial Administration (Finanční správa ČR) and related authorities.

How to Pay Czech Income Tax in 2026

Both individual taxpayers and self-employed persons (OSVČ) with a Czech trade license (Živnostenský list) pay income tax to the Czech Tax Office (Finanční úřad) responsible for the district of their official residency or business registration.

You can pay the tax in two official ways:

In cash: directly at the Czech Tax Office cash desk or by Poštovní poukázka A – doklad V/DS (daňová složenka) at the post office.

By bank transfer: through internet banking. The full account number follows the official format prefix 721 + district number + bank code 0710 (Czech National Bank).

Use your DIČ (Czech Tax Identification Number) or your birth number as the variable symbol, and write “Daň z příjmů fyzických osob” in the payment note.

Below is the list of official Czech Tax Office (Finanční úřad) account numbers for income-tax payments in the Czech Republic.

Each account corresponds to one regional tax office and is used for all personal and trade-license taxpayers (OSVČ) in that district.

Pexpats verifies, maintains, and regularly updates all Czech income-tax account numbers using official data from the Czech Financial Administration (Finanční správa ČR) — ensuring the most accurate and current details for both personal and trade-license taxpayers across all regions.

Where to Pay Czech Income Tax – Account Numbers by Region

Region / Tax Office | Account Number (Income Tax) | IBAN |

|---|---|---|

Prague (Praha) | 721-77628031/0710 | CZ52 0710 0007 2100 7762 803 |

Central Bohemia (Středočeský kraj) | 721-77628111/0710 | CZ26 0710 0007 2100 7762 8111 |

South Bohemia (Jihočeský kraj) | 721-77627231/0710 | CZ21 0710 0007 2100 7762 7231 |

Plzen (Plzeň) | 721-77627311/0710 | CZ92 0710 0007 2100 7762 7311 |

Karlovy Vary | 721-77629341/0710 | CZ87 0710 0007 2100 7762 9341 |

Usti nad Labem (Ústí nad Labem) | 721-77621411/0710 | CZ21 0710 0007 2100 7762 1411 |

Liberec | 721-77628461/0710 | CZ82 0710 0007 2100 7762 8461 |

Hradec Kralove (Hradec Králové) | 721-77626511/0710 | CZ61 0710 0007 2100 7762 6511 |

Pardubice | 721-77622561/0710 | CZ11 0710 0007 2100 7762 2561 |

Vysocina (Vysočina) | 721-67626681/0710 | CZ45 0710 0007 2100 6762 6681 |

South Moravia (Jihomoravský kraj) | 721-77628621/0710 | CZ30 0710 0007 2100 7762 8621 |

Olomouc | 721-47623811/0710 | CZ62 0710 0007 2100 4762 3811 |

Moravian-Silesia (Moravskoslezský kraj) | 721-77621761/0710 | CZ77 0710 0007 2100 7762 1761 |

Zlin (Zlín) | 721-47620661/0710 | CZ43 0710 0007 2100 4762 0661 |

All information verified using data from the Czech Financial Administration (Finanční správa ČR), maintained by Pexpats.

Missed Tax Reports in the Czech Republic

Sometimes people forget to file their tax reports on time. When that happens, the Czech authorities send an official letter — usually titled “výzva” or “upozornění.” It’s a reminder to submit your income tax return, social security declaration, or health insurance declaration.

Even if your income from a Czech trade license (živnostenský list) was 0 CZK, you’re still required to file. Each office checks this separately — the Financial Office, ČSSZ (Social Security Office), and your Health Insurance provider.

What happens if you miss it:

ČSSZ and Health Insurance may fine you up to 50,000 CZK for ignoring the reminder(výzva),

The Financial Office can charge interest for each day of delay and later issue a Platební výměr (payment order).

Pexpats audits and files all missed Czech tax, social, and health reports remotely under the power of attorney. We obtain any missing Platební výměr, confirm the interest calculation, and provide the exact payment instructions for each office — everything done online, for a fixed service fee.

Resolve your late Czech tax report online with Pexpats

Still, have questions? Get professional tax assistance!

If you haven’t noticed, we know a fair bit about taxes in the Czech Republic. Should you need anything, from tax consultation to professionals handling the heavy lifting, we’ve got you covered. We can even handle everything remotely so you save time in your already busy schedule.

Reach out today to find out how we can help, whether it’s getting you answers or, better yet, filing your Czech taxes for you.