Czech Taxes - Important Guidelines and Info for Expats

Freelancers, employees, and companies all must pay taxes on income they receive in the Czech Republic. This is on top of mandatory payments into health insurance and social security, and different rules for self-employment versus employment. Income tax rates are also 15 percent or 23 percent, depending on the annual income of the taxpayer.

However, for self-employed trade license (OSVC) holders, it can be more difficult to navigate Czech taxes than for full-time employees. This is more true for foreigners looking to start freelancing from scratch, or to register a Czech company (s.r.o.). There are different tax rules and regulations, as well as different types of trade licenses. That’s not to mention the freelancer versus employee income tax return, or the types of tax relief, discounts and bonuses.

How do self-employment taxes work in the Czech Republic?

In general, self-employment in the Czech Republic requires a free trade license (“živnostenský list” in Czech, or “zivno” for short). The trade license registers a person for certain business activities, which in many cases do not require special certification. It also provides the person a tax number, and grants them the same rights as a registered Czech company.

There are currently 82 general trade license activities which do not require special education or university degrees. The most common of these are foreign language teaching, IT, graphic design, general consulting, sales, and providing certain services. These include for example: photography services, event management, and similar un-regulated freelance work.

Sole traders are able to perform all 82 of these general business activities at once and under one trade license. This means there is often no need to change or update the license when switching from one profession to another. The only time this would be necessary is if changing to professional trade license activities which the government regulates.

How do I get a trade license in the Czech Republic?

To get a Czech trade license, applicants must submit an official application and required documentation to relevant offices. However, the requirements for this process differ depending on the applicant’s nationality, residency status, and type of trade license

In general, all trade license applicants must:

Be above 18 years old (of full autonomy and able to carry out legal activities)

Have no criminal record (providing proof for some nationalities)

Further, applicants must submit different supporting documents depending on their nationality and residency status.

Note: One of the most important conditions is submitting a criminal clearance report. This report usually comes from the applicant’s home country if they do not already have Czech permanent residency. The process is also easier for some expats such as EU citizens, while non-EU citizens have different requirements.

Trade license criminal clearance report conditions

The criminal clearance report conditions for trade license applicants of different nationalities are as follows.

EU citizens do not need a criminal clearance report or temporary residency to get a trade license.

Ukrainian citizens do not need a criminal clearance report if they have visa protection or foreign police registration. In this case, the temporary protection visa (in Czech, “Dočasná ochrana,” or “vizum strpeni”) fulfills the criminal clearance condition.

Other non-EU citizens with an exception to the criminal clearance condition include holders of permanent residency, a student visa (visa/residency code D/VC/23), partnership visa holders, Blue Card holders, refugees and their family members).

US citizens must provide an affidavit that they sign at the US Embassy confirming they have not committed any crimes. This is because the criminal clearance report does not exist in the US.

Note: The charge for the affidavit is 50 USD.

Canadian citizens must provide a criminal clearance report from Canada (translated into Czech). If doing this from Canada, note it will be necessary to find an official translator and have a super legalization stamp from the Czech Embassy.

Citizens of Australia, Brazil, and South Africa must submit a criminal clearance report from their home country (translated into Czech and with an official stamp of apostille).

Note: Many countries are already issuing digital criminal clearance reports. These documents fulfill the condition as long as they are verifiable by QR code.

Also, the criminal clearance report must be no older than 90 days from the date of issue. Then, after meeting the criminal clearance report condition, full registration of a general trade license usually takes 2 days.

Types of Czech trade license

The two categories of the Czech trade license separate general business activities from professional trade certification. A general trade license is easier to obtain, and is the most common. General trade licenses (OSVC) register the freelancer to:

Provide services from a list of 82 common business activities

Perform their trade often with no proof of specialized education or university degrees

Work in sectors such as graphic design, IT foreign language education, etc

business activities

1. Provision of services for agriculture, horticulture, fishing, forestry and hunting 2. Professional forest management 3. Production of forest management plans and outlines 4. Handling of the reproductive material of forestry plants 5. Animal breeding and training (with the exception of animal production) 6. Treatment of minerals, extraction of peat and mud 7. Manufacture of food and starch products 8. Fruit distillation 9. Manufacture of feed, compound feed, additives and premixtures 10. Manufacture of textiles, textile products, clothing and clothing accessories 11. Manufacture and repair of footwear, saddlery and harness products 12. Wood processing, manufacture of wooden, cork, straw and plaiting products 13. Manufacture of pulp, paper and paperboard and of goods made of those materials 14. Publishing, printing, binding and copying 15. Manufacture, reproduction, distribution, sale, rental of audio and audiovisual recordings, and manufacture of blank data and recording carriers 16. Manufacture of coke, raw pitch and other solid fuels 17. Manufacture of chemical substances, fibres and preparations, and cosmetic products 18. Manufacture of fertilizers 19. Manufacture of plastic and rubber products 20. Glass manufacture and processing 21. Manufacture of building materials, porcelain, ceramic and plaster products 22. Manufacture of abrasive products and other non-metallic mineral products 23. Technical and jewellery stone cutting 24. Production of iron, precious metals, non-ferrous metals and their alloys 25. Manufacture of metal structures and fabricated metal products 26. Artistic and craft working of metals 27. Surface treatment and welding of metals and other materials 28.Manufacture of measuring, testing, navigation, optical and photographic instruments and equipment 29. Manufacture of electronic components, electrical equipment, and the manufacture and repair of electrical machinery, appliances and electronic equipment powered by low voltage 30. Manufacture of non-electric domestic appliances 31. Manufacture of industrial machinerytheir 32. Manufacture of motor vehicles and trailers and bodies 33. Design and manufacture of vessels 34. Manufacture, development, design, testing, installation, maintenance, repair, modification and structural changes to aircraft, aircraft engines, blades, aircraft parts and equipment and aviation ground facilities 35. Manufacture of rail traction units and rail vehicles on tramways trolley-bus tracks and cableways, and railway fleets 36. Manufacture of bicycles, wheelchairs and other non-motor vehicles 37. Manufacture and repair of upholstered products 38. Manufacture, repair and maintenance of sport products, games, toys and prams and pushchairs 39. Manufacture of medical devices 40. Manufacture and repair of sources of ionizing radiation 41. Manufacture of school and office equipment, except paper products, the manufacture of costume jewellery, brooms and brushes, made-up articles, umbrellas, souvenirs 42. Manufacture of other manufacturing articles 43. Operation of water supply and wastewater services, and water treatment and distribution 44. Waste management (except dangerous waste) 45. Preparatory and finishing work, specialized construction activities 46. Glazing, framing and mounting 47. Intermediation in trade and services (Import / Export) 48. Wholesale and retail trade (Shop, online sales) 49. Pawnbroking and retailing in second-hand goods 50. Maintenance of motor vehicles and accessories 51. Transport via pipelines and land transport (except rail and road motor transport) 52. Storage, packaging of goods, cargo handling and technical activities in transport 53. Forwarding and representation in customs procedure 54. Operation of postal and international postal services 55. Accommodation services (Hostel, Pension, Hotel) 56. Provision of software, information technology consulting, data processing, hosting and related activities and web portals (Programmers) 57. Activities of information and news agencies 58. Real estate services, facility management and maintenance (Real Estate) 59. Leasing and loaning of movables 60. Guidance and consulting activities, production of expert studies and opinions (Consultants) 61. Land consolidation design 62. Preparation and production of technical designs, graphic and drawing work 63. Design of electrical equipment 64. Research and development in the field of natural and technical sciences or social sciences 65. Testing, measurement, analysis and inspections 66. Advertising, marketing, media representation (Advertising for 3rd parties) 67. Design and arrangement activities and modelling 68. Photographic services 69. Translation and interpreting 70. Administrative services and services of an organizational and economic nature 71. Operation of a travel agency and guide services in the field of tourism 72. Extra-curricular education, organization of courses, training, including instructor services (Language teachers) 73. Operation of cultural, educational and entertainment facilities, organization of cultural productions, events, exhibitions, fairs, festivals, sales and similar events 74. Operation of physical education and sports facilities and organization of sports activities 75. Domestic washing, ironing, repair and maintenance of clothing, household linen and personal goods 76. Provision of technical services 77. Repair and maintenance of household goods, items of a cultural nature, precision equipment, optical equipment and measuring devices 78. Provision of personal and personal hygiene services 79. Provision of services for the family and households

80. Provision of services for legal entities and trust funds

81. Activities connected to the cryptocurrency and virtual assets

82. Manufacture, trade and services not elsewhere specified

On the other hand, professional trade license certification involves:

Proving competence through special practice or education

Obtaining an official permit to conduct relevant business activities

Job certification for jobs such as taxi cab driving, trades like butchers, bricklayers, or licensed activities: distillery, production, transport, etc

Professional trade license conditions

To expand on above, each type of professional trade license has individual conditions you have to meet for professional certification. In some cases, you will need a special degree or university education, and also some years of experience.

If you don’t have this or other professional certifications, you might have a “responsible person” (in Czech, “odpovědný zástupce”). This person will already have the professional trade license or qualification for the trade you want to perform. They will then be able to sponsor your trade license, becoming responsible for your professional business activities

For example, imagine you want to open a restaurant and hotel, but you don’t have the required education or experience. In this case, another owner, manager, or server might be able to fulfill the trade license conditions. If they can, then they can sponsor your license as the responsible person, allowing you to open the business.

Similar is true for example if you want to start working as a barber or hairdresser. If you don’t meet the necessary conditions, a colleague or a friend with the professional license can become your responsible person.

Trade license registration rules

n addition to the regulations above, trade license holders must also have a business address in the Czech Republic. However, this does not necessarily require you to rent an office space. Usually, Czech-based freelancers register their business at their home address, even when renting. All this requires is proof from the renter that you can legally work out of your residence.

However, there are two disadvantages to using your home address as your business address.

Everytime you move, you need to request permission from the new renter that you can legally work out of the residence. And not every landlord is comfortable signing this paper. In fact, if your new renter refuses to sign, delays in a change of business address can cause problems. For example, the previous landlord can delay refunding a deposit until you have changed your business address.

You have to notify all authorities every time you change your business address. This costs time and money, and can even result in losing official letters if there are any delays.

To make life easier however, it is possible to use a Pexpats’ virtual business address. The virtual address allows you to technically operate your company from Pexpats’ offices in Prague 1. All official communications then go directly through certified accountants and tax advisors who translate and handle your affairs.

In this way, you have both a registered business address, and it’s impossible to miss official communications with Czech authorities. The Virtual Business Address Package comes at a subscription fee of CZK 7,300 per year.

What are the taxes on Czech-based freelancers?

Freelancer (OSVC) taxes in 2026 are 15 percent or 23 percent depending on the amount of taxable annual income. Usually, freelancers determine taxable income using the 60/40 model. This tax option in the Czech Republic enables self-employed workers to automatically deduct 60% of gross annual income as business expenses. The remaining 40% is then taxable at either 15% or 23%, at which point tax relief, discounts, and bonuses can apply.

Other tax options include paying a flat-tax, which is popular as a simpler tax model, or filing actual expenses. The latter obviously involves more accounting, and usually is not the best or easiest way for freelancers to file taxes. That is unless they generate a significant amount of actual expenses, which is not usually the case.

Then, the limit for the progressive 23% tax rate in the Czech Republic is CZK 1,762,812 in 2026. This calculation comes from the average Czech gross salary (CZK 48,967) x 36. Any annual income under this total, and the lower tax rate of 15 percent applies.

How to calculate Czech income tax

On top of the different tax reporting options in the Czech Republic, OSVC freelancer tax rates are quite reasonable and straightforward. But let’s simplify this further, taking for example 2026.

If you want to calculate your Czech income taxes, one way to do this would be as follows.

Determine your taxable clean income using the 60/40 “fixed expenses” tax model. (This automatically deducts 60% of your gross OSVC income, while the remaining 40% is taxable.)

Apply a tax rate of 15 percent or 23 percent to your taxable income. (A tax rate of 15 percent applies to clean income under CZK 1,762,812. The progressive tax rate of 23 percent applies to income over this limit.)

Deduct the standard taxpayer’s discount from your taxable net income. (Note: the standard taxpayer’s discount is available to all taxpayers, and in 2026 is CZK 30,840.)

Claim any tax relief, discounts, and bonuses if you are eligible to do so. (For example: claiming tax credit for having a child or an unemployed spouse.)

Calculate the remaining balance, if any. (Note: If you go into negative here, you owe zero income tax and may in fact be eligible to get money back from your tax return.)

Keep in mind, this tax reporting option also does not require any proof of invoice or receipts. It is available to all freelancers, and you can also claim multiple tax discounts and bonuses on the tax base. In this way, the tax burden is minimal, and the accounting can be easier in general.

Self-employed income tax example

How about some real numbers so you can check our math? Let’s take for example Jane, who had CZK 300,000 self-employed income last year. Using the 60 / 40 model, Jane’s personal income tax return would be as follows.

CZK 300,000 * 60% = CZK 180,000 (fixed expenses)

CZK 120,000 * 15% tax rate = 18,000 (tax base)

CZK 18,000 - 30,840 (automatic taxpayer’s discount) = zero owed to income tax

In this way, Jane needs to pay zero tax on her income from the previous year. She also enjoys one of the most convenient and often best tax options for OSVC freelancers.

Important OSVC tax rules

The 60/40 tax option if your annual income is less than CZK 2 million.

Any taxpayer who earns over CZK 2,500,000 must register for Czech National VAT.

If you invoice any EU-registered business, you must register for Light VAT.

Czech income tax deadline and how to file

The deadline for tax returns in the Czech Republic is generally around April each year. However, if submitting electronically, the deadline extends by one month. In 2026, for example, the deadline to submit the standard tax return is 1 April 2026 (or 4 May 2026 for electronic submissions). The deadline can change from year to year, as we saw during the Pandemic, but for the most part stays the same.

Overview of Czech Income Tax Filing and Payment Deadlines (2026)

Submission Type | Tax Return Deadline | Payment Deadline | Requirement |

|---|---|---|---|

Paper submission | 1 April 2026 | 1 April 2026 | Standard filing |

Electronic submission | 4 May 2026 | 4 May 2026 | Filed online |

Via tax advisor | 1 July 2026 | 1 July 2026 | Power of attorney submitted by 1 April 2026 |

Source: Finanční správa ČR

Self-employed persons, employees, pensioners, students, and anybody responsible for reporting taxes then share the same deadline. You declare income, health & social payments, deductibles or tax credits, and the remaining balance to pay in taxes. All of these, you then submit to the Czech Financial Administration (by mail, in-person, or digitally).

But, why do it alone? Consider Pexpats’ Income Tax Package to get tax advice from a personal certified accountant, including 100% remote adn online filing of your personal income tax return.

How much are Czech Social Security deposits?

Trade license holders must also register with the Czech Social Security Office, and make monthly advance deposits into social security. However, keep in mind that you may also need to pay a remaining balance at the end of the year if you earn over a certain limit.

Note: In 2026, the minimum monthly advance deposit for social security increases to CZK 5,050 (CZK 60,060 minimum per year).

Again, remember that if you make over a certain amount, you will still need to pay a balance in the future. Thus, if you expect to earn higher, consider voluntarily paying more in advance deposits each month. Doing so will help to offset any balance remaining at the end of the year.

How much are Czech health insurance deposits?

Trade license holders in the Czech Republic must also register with and make monthly advances to health insurance. In 2026, the minimum payment for health insurance is CZK 3,306 per month. (CZK 39,672 minimum per year).

This rate applies to freelancers insured through Czech public providers such as VZP, OZP, or VoZP. However, only some freelancers are eligible for public health insurance (VZP), while others have to get private health insurance (PVZP).

The following types of trade license holders are eligible for public health insurance:

EU Citizens (and their family members)

Expats with permanent residency in the Czech Republic

Citizens of the US, Albania, Israel, Tunisia, Turkey, Northern Macedonia, Serbia, Syria, Monte Negro, Japan

Meanwhile, internationals of a different status will need private health insurance coverage.

Note: In 2026, minimum health insurance payments increase to CZK 3,306 per month. (CZK 39,672 minimum per year). And just as with social security, keep in mind these payments remain mandatory even if reporting zero OSVC income

Zivnost OSVC sickness insurance

In 2026, sickness insurance is still optional ( not mandatory) for self-employed trade license holders. If you decide to pay for sickness insurance, note that:

The amount for sickness insurance has increased in 2024 from 2.1% to 2.7%.

Minimum monthly deposits for Czech sickness insurance are CZK 243 per month in 2026.

There is also still no minimum mandatory sickness insurance for trade license holders, such as for health and social obligations.

How the Czech flat tax option works

Since 2021, the Czech Financial Office has introduced a flat tax option for OSVC freelancers. This option is available for trade license holders who decide to forego the annual income tax report. Instead, you pay a monthly advance at a flat rate which covers mandatory payments to social, health, and income tax. There is also no paperwork to submit, and less legwork in general.

In order to register for the flat tax option, the OSVC freelancer must earn under CZK 2 million. The monthly rates are then divided into tax rate bands, according to annual income limits and deductible expenses.

However, be aware that sometimes it is not advantageous to register into a flat tax regime. For example, registering for flat taxes makes more sense for single entrepreneurs. This is due to the fact that they often have fewer tax discounts and bonuses they might be eligible to claim, such as for having children.

Also, there are still many unclear situations around the flat tax option as it remains a pilot project. Thus, authorities are unprepared for all scenarios and questions that arise from this way of reporting taxes.

For example, how can you prove your income or tax declarations as a flat tax payer if necessary? With flat taxes, as there is no paperwork, there is currently no way because you do not file a tax return. This can cause problems in cases of applying for tax residency status, or when renewing residency or a trade license.

Flat tax rates and monthly payments

In 2026, the flat tax rate bands are as follows:

For flat tax rate band 1: the monthly payment is CZK 9,984. (covering monthly installments for income tax at CZK 100; social insurance at CZK 6,578; and health insurance at CZK 3,306 )

Flat tax rate band 2: the monthly payment is CZK 16,745. (This covers monthly installments for income tax at CZK 4,963; social security at CZK 8,191; and health insurance at CZK 3,591.

For flat tax rate band 3: the monthly payment is CZK 27,139. (This covers monthly installments for income tax at CZK 9,320; social security at CZK 12,527; and health insurance at CZK 5,292).

Remember: Always consider professional tax advice to determine if the flat tax option is advantageous in your case.

How to report shared income in the Czech Republic

If you have a cooperating person in your business, part of your income is transferable to reduce your tax burden.

To claim a cooperating person, by law, the person must:

Help with part of your business activities (e.g. administration, accounting, invoicing, customer orders, communication, etc)

Reside and work in the same household or participate in a joint “family business” (as per Section 700 of the Labour Code)

Be a partner or spouse on parental leave, or in some cases a retired parent or child over 18 who is also enrolled in school

Further, if the cooperating person is not on parental leave, their primary source of income must come from your business cooperation. In other cases, this cooperation falls under secondary, independent earnings, making it less advantageous due to additional social security and health insurance requirements.

How to declare a cooperating person

To declare a cooperating person, it is necessary to inform the tax office, social security, and health insurance. The cooperating person must also then register for personal income tax, and have a registered Tax ID number. They will then be able to create a variable symbol with social security and health insurance to make monthly advances.

What are the limits on sharing income?

Per the Income Tax Act, you must transfer the same percentage of income and expenses to the cooperating person. In other words, if you transfer 50% of your income, you must also transfer 50% of your expenses.

The maximum transfer limits on shared income are then:

50% income and expenses (maximum CZK 540,000) for a cooperating spouse

30% income and expenses (maximum CZK 180 000) for a non-spouse

Further, it is possible to have more than one business partner. But, in this case, you can transfer only 30% of your total income and expenses across all cooperating persons.

Example of reporting shared income

Let’s look at an example of how sharing income with a cooperating person in the Czech Republic can be advantageous.

Say you earn CZK 800,000, and you use the 60/40 option without a cooperating person.

This gives you CZK 480,000 fixed expenses, and a clean income of CZK 320,000.

CZK 320,00 * 15% tax rate = CZK 48,000 taxable income (before applying the standard taxpayer’s discount of CZK 30,840).

In this case, after the standard taxpayer’s discount, you owe CZK 17,160 in the end.

Compare that to if you declare, for example, a spouse as a cooperating person.

Here, you transfer 50% of your income and expenses to your spouse. (Note: the spouse’s main employment is from your business).

Now, both tax returns become the same: CZK 400,000 profit and CZK 240,000 expenses, with an income tax of CZK 24,000 to pay.

Apply the standard taxpayer’s discount of CZK 30,840 to the owed income tax of CZK 24,000 = zero income tax to pay for both you and the spouse.

CZK 24,000 - 30,840 (standard taxpayer’s discount) = zero income tax to pay for both you and your spouse.

This way you not only reduce your tax burden. You also ensure your spouses’ income does not exceed the taxable base after discounts, so both persons have zero tax liability.

Taxes on Side Income

If self-employed as a secondary activity in the Czech Republic, any extra income on top of your salary is taxable. The tax rate then depends on your main source of income, and the tax base from your trade license.

Also, if it is your first year of earning side income, you will not make any additional monthly payments to social and health. This remains the responsibility of your employer until the end of the first year. After the end of this taxable period, you will then request an annual statement from the employer

At this point, you might have to pay a remaining balance if earning above a certain threshold on your trade license. Note: You can still use the 60/40 tax option. However, if claiming tax bonuses or discounts through full-time employment, you will pay full income tax from the taxable amount.

For example, in 2026, the limit on social tax is CZK 117,521. If you report a clean income higher than this limit, you then pay a remaining balance and begin paying deposits the following year. The monthly advance deposit for side income is CZK 1,574 per month, which goes towards the next taxable year’s mandatory contributions.

If your clean income ( 40% of your gross income) is CZK 117,521, then you pay 0 social tax.

Social tax for students, pensioners, and maternity leave

For students, pensioners, and parents on maternity leave, the social tax limit is CZK 117,521. If your annual net income is lower than this amount, you will not owe anything to the social tax.

Also keep in mind that your annual net income is 40% of your gross annual when using the 60/40 method. Then, if earning above the threshold, you will pay the full social tax, and start making monthly advance deposits.

How much is taxation on student freelancers?

Taxation for students working on a trade license is the same as for all freelancers. Students can file taxes using the 60/40 method, and have a tax rate of 15 percent or 23 percent. Student income is then considered side income, with the minimum CZK117,521 net income rule. All registered trade license holders then must:

File an income tax report at the end of a taxable calendar year.

Declare taxable income from the previous year.

Report advance deposits to social security and health insurance.

Pay income tax as well as any remaining balance to social and health (if any).

Students qualify for a freelance tax discount which is CZK 30,840.

Corporate (s.r.o.) tax in the Czech Republic

The s.r.o. (in Czech, “Společnost s Ručením Omezeným”) is a limited liability company (LLC). It is one of the most common commercial business types, and is often beneficial for small to medium size businesses. This is because of the personal liability protections and flexibility that comes from an LLC (s.r.o) business structure.

For example, a Czech s.r.o. might have multiple official shareholders, founders, CEOs, and managing directors. These partners are then only liable for the company’s obligations up to their original contribution to the company. In the Czech Republic, the s.r.o. must also register a minimum amount of capital to start the business.

Corporate s.r.o. Income tax is 21% of Income in 2026 in the Czech Republic.

If curious to learn more, don’t miss the complete guide on how to register a Czech Company.

Gift tax in the Czech Republic

As per the Income Tax Act, there has been no gift tax or inheritance tax in the Czech Republic since 2014. Instead, taxpayers must declare all donations together in their annual income tax report. Donations are then taxable at a 15% rate for OSVC freelancers, while legal companies pay a 21 percent tax rate.

Further, assets from donations are subject to zero gift tax, and are declarable under gratuitous income. This income has the same tax rate as all other income from one tax year to the next.

Tax-exempt gifts in the Czech Republic

Gifts from a spouse or direct relatives (children, parents, grandparents, grandchildren)

Donations from a collateral line of kin (siblings, nieces, nephews, uncles, aunts; children’s spouses; spouse’s children, spouse’s parents, parent’s spouses)

Gifts from somebody who lived with the beneficiary, donor, or testator for at least 1 year before the transfer or death of the testator in a joint household. This person was thus either a caretaker of the joint household, or was once a dependent of the beneficiary, donor, or testator for maintenance purposes

Note: Any donation that does not exceed CZK 15,000 per year (tax period) is exempt from income tax. This stands regardless of the donor.

Taxes on the transfer of real estate

As for Czech taxes on selling real estate, the same gift tax rules as above apply. For example, selling a house, apartment or flat is exempt from gift taxes, but instead falls under income tax. That is, unless you are one of the above groups, in which case the property is tax exempt. If not exempt, freelancers pay a 15% tax rate on property they sell, and legal companies pay 21 percent. This amount files as gratuitous income, and will have subsequent tax rates from year to year

Also, there are a few other tax exemption rules when selling a house, flat, or other property in the Czech Republic. For example, let’s say you are selling an apartment which you bought a few years ago. You bought the apartment for CZK 2 million, and are selling it for CZK 3 million. In this case, you earned CZK 1 million, and should technically pay 15% tax on that income. That is, unless the property meets tax exempt conditions.

The conditions in which the sale of a house or apartment in the Czech Republic are tax exempt are:

You have owned the property for at least 10 years.

You have lived in the house or apartments for at least 2 years (and are registered there).

You intend to buy another property with the income, and intend to live there.

If you meet any one of the above conditions, there will be no income tax you owe on the sale of the property.

Curious to see how much rental tax you’ll pay for renting a house or flat in the Czech Republic? Use the Pexpats’ Online Czech Rental Income Tax Calculator to calculate your income taxes and annual net income from renting property.

Crypto and Capital Gains Tax Rules in the Czech Republic (2026 Update)

Since February 15, 2025, the Czech Ministry of Finance has confirmed updates that make the Czech Republic one of the few EU countries where crypto and investment profits can be entirely tax-free, provided certain conditions are met. These rules apply to both private investors and freelancers with a Czech trade license.

Tax-free crypto and capital-gains income applies in two main situations:

1. Long-term holding — over three years

When cryptocurrency or investment assets are held for more than three consecutive years, any profit from selling them is exempt from personal income tax.

Example: An investor who bought Bitcoin in 2021 and sells it in 2026 pays 0 % crypto tax, regardless of how much profit is made.

2. Annual profit under €4 000

If your total profit from crypto during the year does not exceed €4 000, no tax is due — even if the holding period was shorter.

Example: Buying Ethereum for €4 000 and selling it the same year for €7 900 creates a gain of €3 900. Since the profit is under the €4 000 threshold, it remains tax-free.

3. Investment and capital-gains exemption

The same three-year rule applies to shares, ETFs, and other securities. After this period, any capital gain becomes fully tax-exempt.

If your profits don’t fall within these exemptions, they must be included in your annual income tax return.When you report crypto or investment profits under your Czech trade license, these amounts are added to your overall freelance income and taxed together.

Unlike your regular business income, though, no social or health insurance is paid on crypto or capital gains — only the income tax applies.

Need to know if your crypto income qualifies for 0 % tax in the Czech Republic? Use the Pexpats Crypto & Capital Gains Calculator — it’s free of charge, works 100 % online, and instantly shows whether your profit falls within the tax-free range.

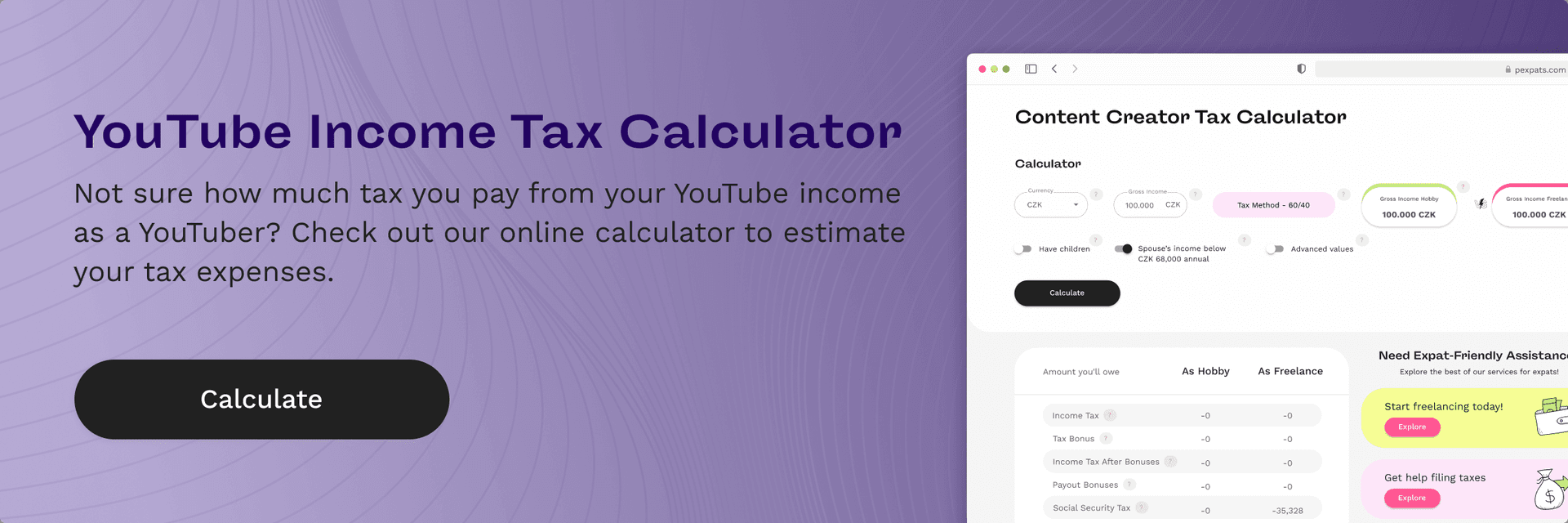

Czech taxes on YouTubers and media creators

If selling or producing content that generates income online, all of this income is taxable in the Czech Republic. This includes income from subscription-based content platforms, online private content, and any media that generates revenue from views or ads. We’re talking about YouTube, OnlyFans, and similar online social or private platforms.

Any digital content income such as this, you can declare as either self-employed income, or as hobby income. However, know that when declaring hobby income, it is not possible to file using the 60/40 tax method. Instead, you have to declare your total earnings, and then pay either the 15 percent or 23 percent income tax rate. In this case, tax discounts and bonuses can still apply, and there are no mandatory deposits to social security or health insurance. Hobby income is also VAT-free in the Czech Republic.

On the other hand, declaring income from digital media on a trade license allows you to use the 60/40 method. But, this is in addition to the OSVC requirements to social security and health insurance. It is also with the same tax rates as OSVC freelancers, with the income limit for the progressive 23 percent rate at CZK 1,762,812 in 2026.

Want to compare taxes on digital media when declaring as a freelancer versus as a hobby? We’ve got a calculator for that, too!

When to file an employee income tax return

There are many cases in the Czech Republic when it makes sense to file an employee tax return, and others when it’s mandatory. For one, employers are not responsible for declaring any tax relief, discounts, or bonuses you may be eligible to claim. Instead, employers often apply only the standard taxpayer’s discount to their employees’ tax returns.

This ignores for example tax discounts for having an unemployed spouse, or for raising children. In order to apply for these, full-time employees should voluntarily file their own tax return. And this requires a “confirmation of taxable income from dependent activity.”

The confirmation should cover the entire taxable calendar year, and all employment during that time. Further, you should report any additional income over CZK 6,000 per year. The employee tax return should then declare your total income (including other earnings, gifts, or inheritance). This will include any tax relief, discounts, or bonuses you can claim.

Most commonly, you might file an employee tax return for example to declare side income that you must legally report, or an inheritance. In other cases, it might be for example working for two employers at once, earning above standard income, or declaring capital gains. All of these require you to submit the annual employee tax return.

Not sure if you need to file an employee tax return by law, or how much you can receive if doing so? Find out now using Pexpats’ online, Czech Employee Tax Return Calculator.

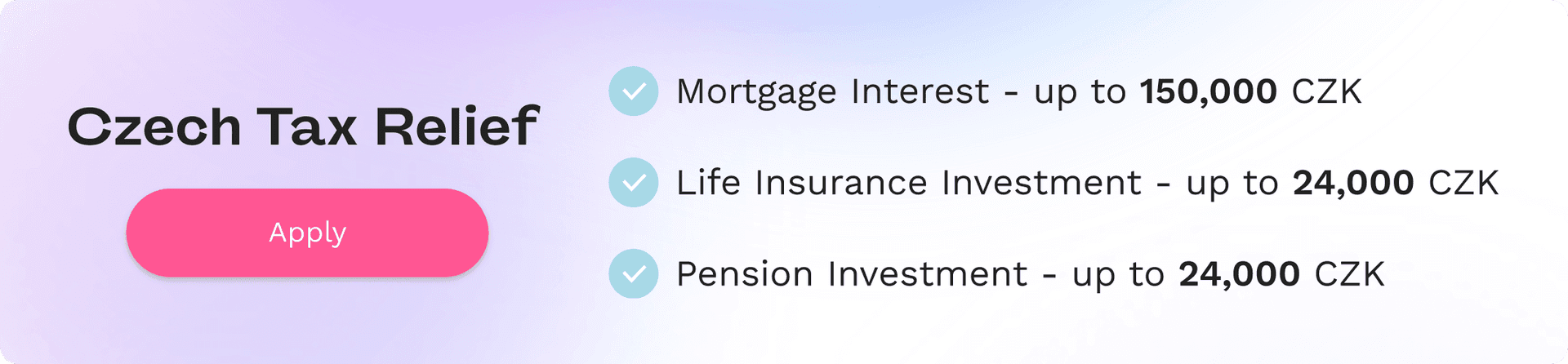

What tax relief is there in the Czech Republic?

Tax relief is the expenses deductible from taxable income (your tax base). In other words, if using the 60/40 tax option, your tax relief applies to the 40% base you pay taxes towards.

In 2026, tax relief is applicable if the freelancer’s clean income is higher than CZK 134,400. Business expenses you can write off then include:

Voluntary Blood, Plasma, or Organ Donor Relief (for voluntary blood, plasma, or organ donors who opt not to get paid) - CZK 3,000 for blood; CZK 3,000 for plasma, or CZK 20,000 for plasma

Mortgage Interest Rates Relief (for the months which you have an active trade license while also paying on a mortgage) - up to a maximum deductible amount of CZK 150 000

Pension and Retirement Funds (for private pension savings within the non-government sector) - up to a maximum deductible amount of CZK 24,000 from private pension savings investments

Life Insurance - up to a maximum deductible of CZK 24 000 for life insurance payments

Continuing Education Examination Fees (for examination fees to certify an improved / progressing level of education) - up to a maximum deductible amount of 10 000 CZK

Research (for implementation of public research and development - no limit to the deductible amount

Supporting Professional Education (for any related expenses to support the education of another person: tuition, exam fees, etc) - no limit to the deductible amount

What tax discounts are there in the Czech Republic?

Unlike tax relief, a tax discount is an amount you deduct from the total tax amount (not the tax base). In the Czech Republic, the tax discounts are:

The standard taxpayer’s discount. This discount is available to all freelancers, no matter if your trade license has been active the full year or only a month. In 2026, the standard taxpayer’s discount is CZK 30,840. It applies to all income from self-employment, regardless of whether it is the main source of income or side income.

A tax discount for an unemployed spouse (or a spouse with income under CZK 68,000 annual net). This discount is available to all taxpayers as long as the spouse meets the above conditions.

Spouse Tax Discount Rules:

The spouse discount applies only for full months of marriage in the previous tax year.

Example: If the marriage started on 30 November, only December is considered a full month. In this case, you can claim 2,040 CZK for that month.

The spouse tax discount can be claimed only for the months the spouse lived in the Czech Republic.

Example: If your spouse moved to the Czech Republic in February, you can claim the spouse discount for 11 months (February–December).

Most Common Tax Discounts 2026

Type of Tax Discount | Who Qualifies | Tax Discount Amount | Rules |

|---|---|---|---|

Freelancer Tax Discount | All self-employed people | 30,840 CZK/year | You get the full 30,840 CZK even if the trade license was active only part of the year. |

Spouse Discount | Married taxpayers with a spouse earning under 68,000 CZK/year | 24,480 CZK/year | Spouse must provide daily care to a child under 3; applies only for full months of marriage |

What are the tax bonuses for having children?

The tax bonuses for having children are an amount you can claim back in your annual income tax return. This amount includes tax bonuses for parents of one, two, or more children.

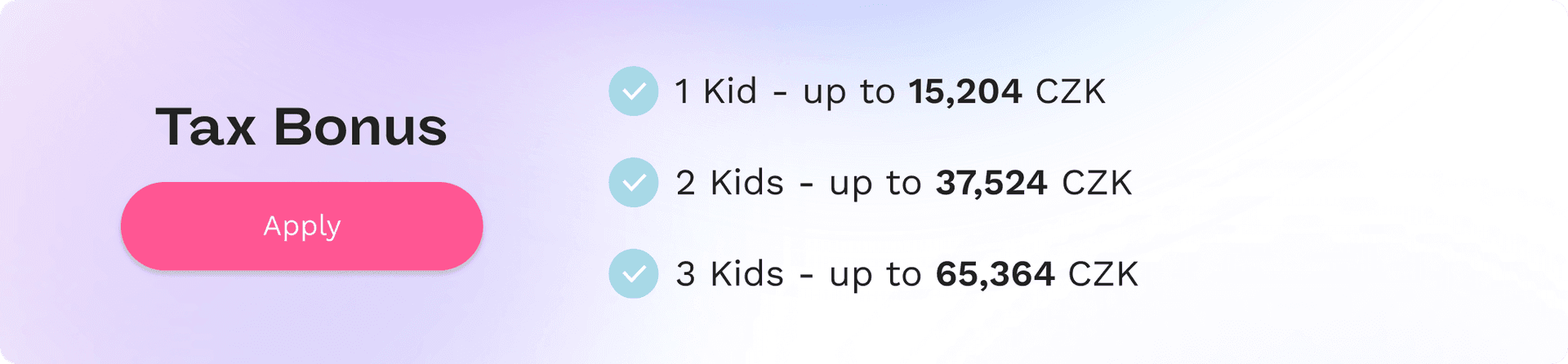

For the first child, the maximum bonus is CZK 15,204.

For a second child, the maximum bonus is CZK 22,320.

For three or more children, the maximum bonus is CZK 27,840.

Czech Child Tax Binus rules

Only one of the parents can claim a tax bonus for children.

The length of your trade-license activity does not affect eligibility for the child tax bonus. If the child existed for the full year but your trade license was active for only one month, you can still claim the full yearly bonus.

Example: If a child was born on 30 November, only December counts as a full month. You can claim 1/12 of the yearly amount (for a first child: 1,267 CZK).

The Czech child tax bonus can be claimed only for the period the child lived in the Czech Republic.

Example: If you moved to the Czech Republic with your child in June, you can claim the child bonus only for 7 months (June–December).

Advance tax payments in the Czech Republic

In the Czech Republic, it may be necessary for you to make advance tax payments. However, this requirement is only for taxpayers who paid over a certain limit of income tax in the previous year. Advance tax is income tax that you pay in advance through deposits rather than paying a lump sum.

Instead, you make advance deposits semi-annually or annually towards an expected tax amount. This is even if you are unable to calculate your tax liability in advance. You will then settle any balance remaining, minus the advanced payments at the end of the tax period.

Who does not need to pay advance tax?

You do not need to enter into the Czech advance tax system if:

You paid CZK 30,000 or less income tax in the previous financial year.

Your business or self-employment is in its first year of legal activity.

You have full-time employment (in this case, your employer pays the tax advance).

You’re registered for the flat tax option.

Again, remember that the flat tax option is not going to be advantageous for all freelancers. It is a special tax option that can greatly simplify reporting, but comes with both advantages and disadvantages.

When do you need to pay advance tax in the Czech Republic?

If your income taxes were CZK 30,000 or higher in the previous year, you must pay advance tax. Note that the limit is after any tax relief, discounts, and bonuses you were eligible to claim.

The amount of the advance deposits and their payment deadlines then depend on your most recent tax liability. Again, this will be how much income tax you paid after all deductions and discounts, such as for having children.

How much are advance tax payments?

If you are an advance taxpayer in the Czech Republic, the deposit amount falls into two categories. These include tax deposit limits according to total tax liability, and the advance tax rates which apply. The two advance tax deposit categories are:

Semi-annual advance deposits. These are for if you paid more income tax than CZK 30,000 but less than CZK 150,000. If this is your case, advance deposits will be 40% of your tax obligation, and you pay these twice per year.

Quarterly advance tax payments. These are for if you paid higher than CZK 150,000 income tax in the previous financial year. In this case, you pay 25% of your tax obligation four times per year.

Semi-annual advance tax deposit example

Now, for the math behind the semi-annual advance tax deposit:

Say that you paid CZK 100,000 income tax last year.

This means you make advance tax deposits semi-annually (2x per year).

The amount of the semi-annual advance tax is then 40% of the original income tax you paid, amounting to CZK 40,000.

CZK 40,000 x 2 payments (subject to due dates) = CZK 80,000 total tax advance payment for the year.

If for example you owe CZK 100,000 again this next year, you will have CZK 20,000 balance remaining. This you will pay at the end of the financial year.

Quarterly income tax advance example

ake the following example for quarterly income tax advance deposits in the Czech Republic:

You paid in total CZK 200,000 income tax last year.

The advance tax threshold obligating you to make quarterly payments is CZK 150,000.

This means you make payments 4 times per year.

The amount of the quarterly advance tax is then 25% of the original income tax paid.

CZK 50,000 x 4 payments (subject to deadlines) = CZK 200,000 total advance tax payments.

If for example you owe CZK 200,000 again this next year, you will have zero balance remaining. If you owe anything more to income tax you will pay the final balance at the end of the financial year.

When are the advance tax payments deadlines?

Deadlines to make tax advance deposits depend on if you make semi-annual or quarterly payments. The payment deadlines are then:

15 June and 15 December (for semi-annual advance tax payments)

15 March, 15 June, 15 September, 15 December (for quarterly payment deadlines)

Should you register for VAT or Light VAT?

Trade license holders may also need to register as a VAT payer, or as a Light VAT payer. However, this is only in certain conditions. These include earning above CZK 2.5 million, or regularly invoicing EU-registered business clients outside of the Czech Republic.

You may also need to register into the VAT system for selling certain goods and services, which then fall under different VAT rates.

What are the Czech VAT rates?

n 2026, there are two Czech VAT rates (the standard 12 percent, and the progressive 21 percent). These replace the three VAT rates of 2026 (the second reduced 10%, the reduced 15%, and the progressive 21%). This should simplify the VAT system by unifying the previous two reduced rates into one reduced rate of 12 percent.

Also, there is a zero VAT rate on books, and lower food product rates than in 2023. Bus and irregular transport is also down from 21% to the reduced 12 percent rate. This is with higher rates on beverages, certain services, and draft beer.

Note: Items which VAT Law (in the reduced VAT section) does not mention, will have the standard 21% VAT rate.

Want to see exactly how much VAT to add on your Czech invoices? Use Pexpats’ VAT Payment Calculator to experiment, and to find answers to frequently asked VAT questions.

How to register as a Light VAT payer

If you regularly invoice EU-registered business clients outside of the Czech Republic, you should register for Light VAT. In other cases, it may even be advantageous for you to voluntarily register for Light VAT. Keep in mind, registering for Light VAT does not mean you will pay extra VAT.

Your VAT will always be zero with Light-VAT invoices. However, to invoice this way, you have to apply for Light VAT on a monthly basis through the relevant Financial Office. This informs the tax office that business is happening between a Czech business and a registered EU company.

Note: It is only possible to register for Light VAT after you have a business license in the Czech Republic. You must then register for Light VAT after you create the first invoice for an EU-registered business-client.

At this point, the tax office will need to approve your invoices on a monthly basis. This requires you to create a formal request every month, which you then submit to the financial authorities.

Not sure if your VAT number or a client’s VAT number is valid? A quick check of the VAT Number Checker can verify any registered VAT payer in seconds.

How to create a Czech invoice online

The easiest way to create your first Czech invoice is using Pexpat’s online invoice generator. This free invoicing tool creates invoices in Czech or English language, and autofills information by company’s ID number (ICO). Simply enter the details for you and your client, and the generator takes care of the rest.

Better yet, take advantage of a free user account for even more financial tools and quicker invoicing. User accounts allow you to record client details, archive invoices, autofill exchange rate text, light VAT, and invoice numbers. All with payment reminders, bank details you can save as you invoice, and multiple bank accounts for invoicing in different currencies.

Online Czech tax calculators

To take the guesswork out of Czech taxes and your overall finances, Pexpats has many completely free-of-charge online tax calculators. These help you to quickly calculate what you’ll earn and owe in the Czech Republic. Find everything from net salary to income tax calculators, and even tools to better understand maternity pay or holiday allowance.

Better still, we keep everything up-to-date and include frequently asked questions so you always have accurate tax and payment information.

Need professional help filing a Czech tax return?

Do you have more questions about Czech taxes and filing that annual tax return? At Pexpats, our certified tax accountants work from the heart of Prague 1, and are available in-person or 100% remotely.

Our team provides advice and professional tax services for internationals, freelancers, and employees, no matter how complex the situation. Curious to learn more? Just let Pexpats know how we can help, and one of our agents will get right on your case!